Silicon Valley Market Update: September 2022

October 1, 2022

Market Update

October 1, 2022

Market Update

Our team is committed to continuing to serve all your real estate needs while incorporating safety protocol to protect all of our loved ones.

In addition, as your local real estate experts, we feel it’s our duty to give you, our valued client, all the information you need to better understand our local real estate market. Whether you’re buying or selling, we want to make sure you have the best, most pertinent information, so we’ve put together this monthly analysis breaking down specifics about the market.

As we all navigate this together, please don’t hesitate to reach out to us with any questions or concerns. We’re here to support you.

– Brian Ng & Thao Dang, LIC #01348634 / 00846794

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

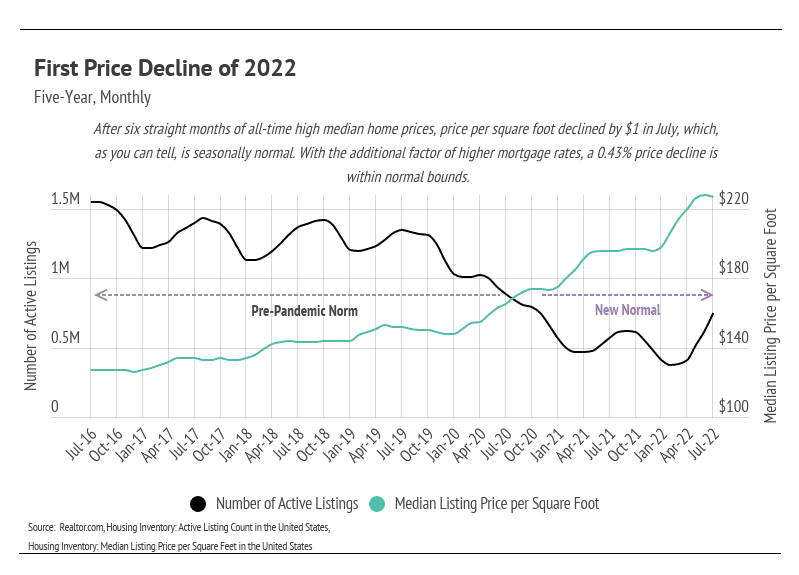

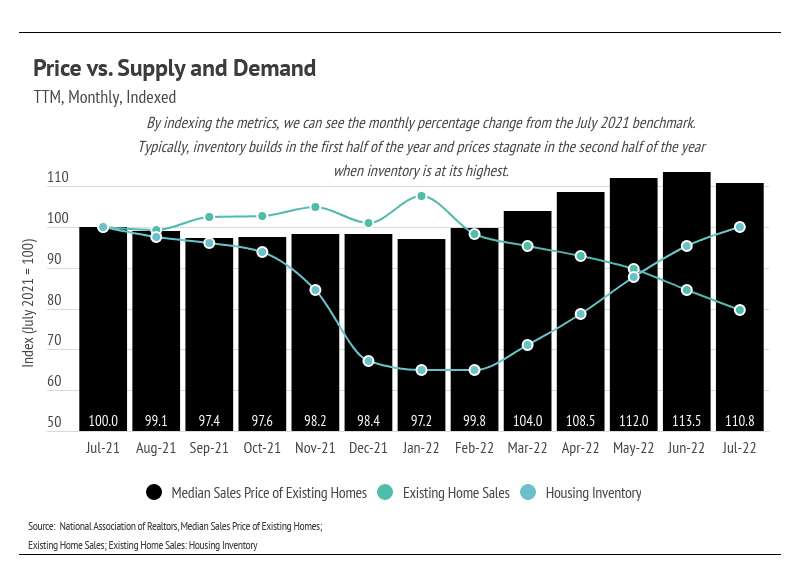

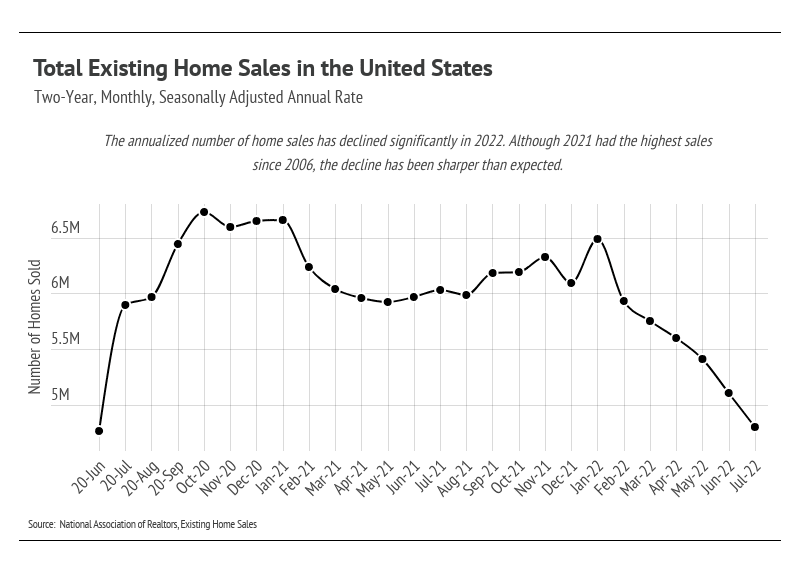

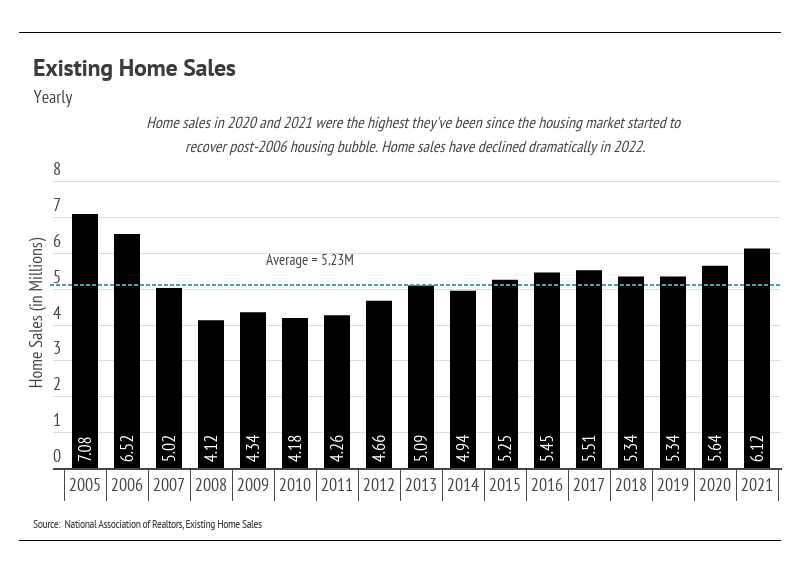

We knew the end of the streak was coming. Higher mortgage rates, which negatively affect affordability, combined with the typical summer sales slowdown and higher inventory have caused prices to decline month-over-month from the all-time high they reached in June 2022. The National Association of Realtors (NAR) data show that the median home price in the United States declined by 2.4%, and Realtor.com data indicate that the median price per square foot declined by 0.43%. These aren’t major declines, as you can see, especially when considering the decline in sales. According to NAR, the number of homes sold dropped 5.9% month-over-month and 20.2% year-over-year, which is substantial but not necessarily unexpected. Home sales in 2020 and 2021 were the highest since the 2006 housing bubble burst, which set the stage for the 2008 financial crisis, and normal seasonal trends were less pronounced or non-existent. It’s very easy to get wrapped up in the recent past, especially when it comes to large financial purchases, most of which (a new home!) are profoundly life-changing. We weren’t sure how long the break in historic seasonality would last, but it seems to have ended, and seasonality has mostly returned.

As we look at the pre-pandemic seasonal trends, home prices and inventory increased in the first half of the year and declined in the back half. The trend is essentially two steps forward and one step back over and over, so even when the second half of the year sees some price decline, year-over-year prices tend to be higher. In July, we reached the longest-running streak of year-over-year home price increases on record, with 125 consecutive months. This year, inventory may peak later than usual if sales continue to decline through what are typically the strongest sales months (May-August). From January 2020 to June 2022, the median price per square foot rose 54%, so there is definitely room for some price declines in the back half of this year.

The monster price gains in 2020-2022 were, of course, pandemic related, and the already tight housing supply dropped to shockingly low levels. However, with fewer sales than expected and more new inventory coming to market, active listings have nearly doubled from the all-time low reached in February 2022. More inventory can only benefit the market, as we are still 44% below July 2019 (pre-pandemic) levels. Housing starts have declined since this past April as the cost of building has gone up. The National Association of Homebuilders’ Housing Market Index, which measures homebuilder sentiment for the single-family home market, has declined every month of 2022. These declines in sales and home building have led NAR Chief Economist Lawrence Yun to use the term “housing recession” with some caveats. We believe, however, that the word “recession” is too dark a picture for the current market. Although the market still favors sellers over buyers, we are moving toward a more balanced market, which feels like quite a switch given how deeply we dove into a sellers’ market since mid-2020. The market is getting healthier and a little less hot, which is ultimately beneficial to everyone participating when we look at the big picture. Buyers are facing less competition, but they still must compete, and sellers are still generally getting at least asking price.

The U.S. housing market has become more nuanced over the past several months, depending on the region. Some parts of the country are trending closer to balance, while some are moving deeper into a seller’s market. Take a look below at the Local Lowdown for in-depth coverage of your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Quick Take:

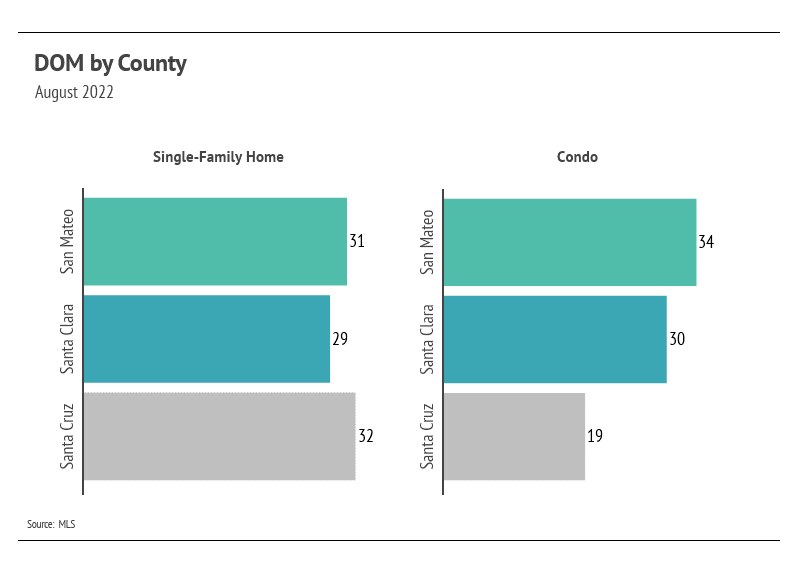

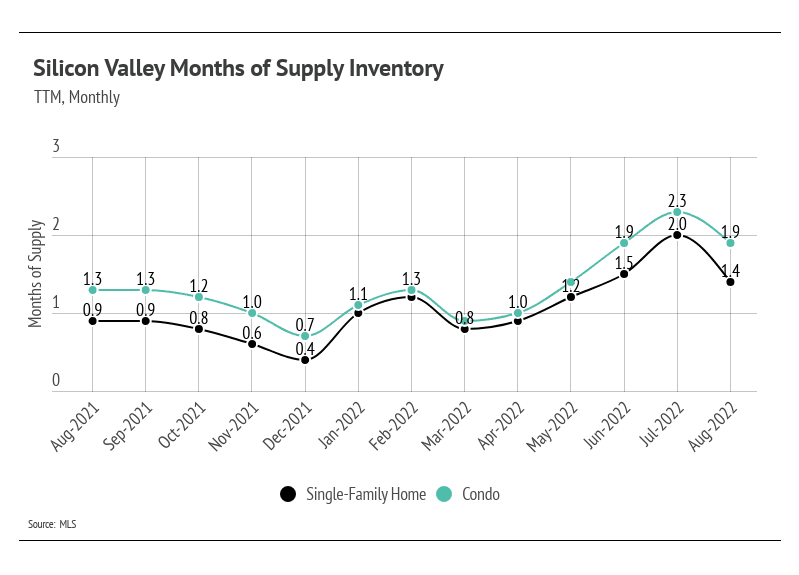

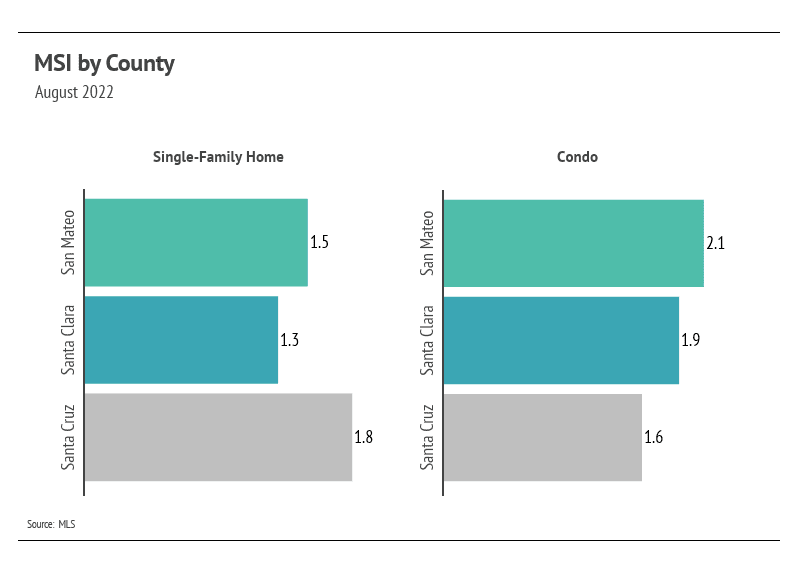

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

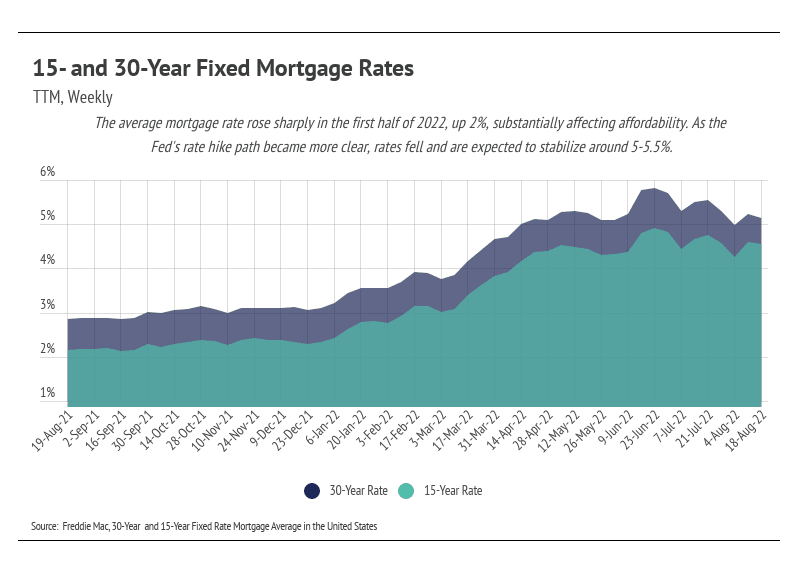

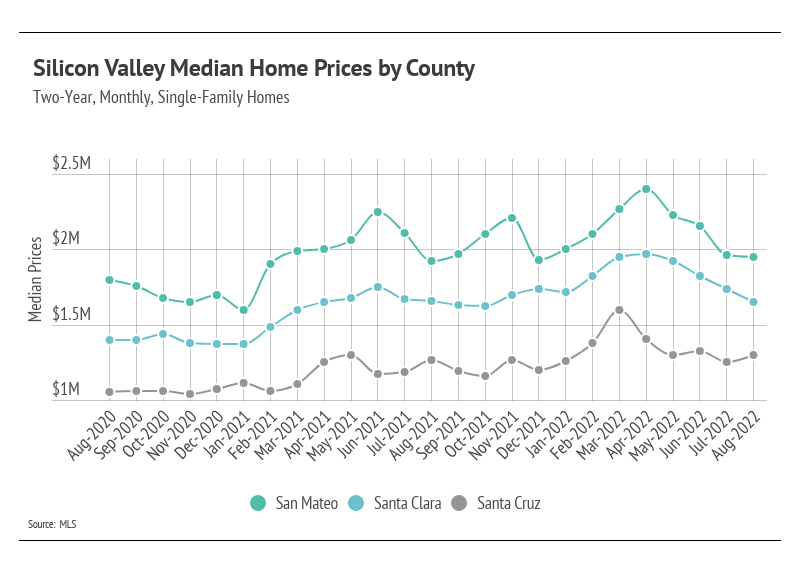

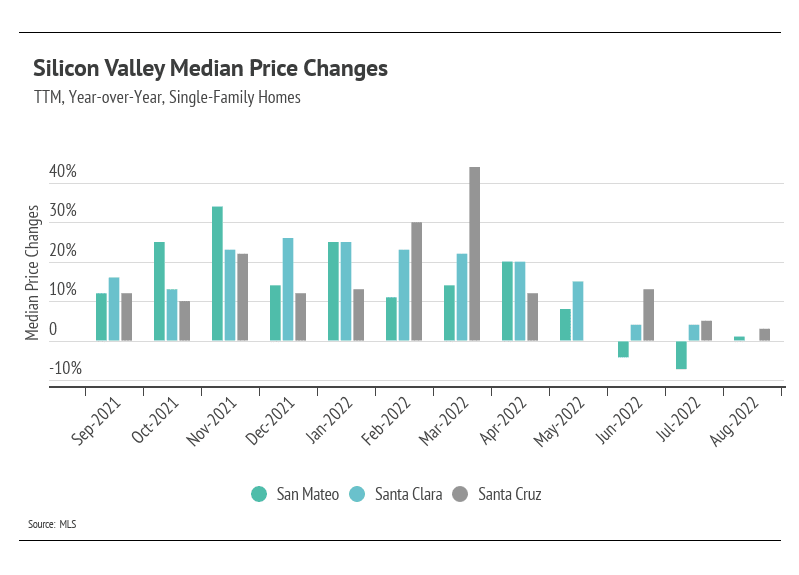

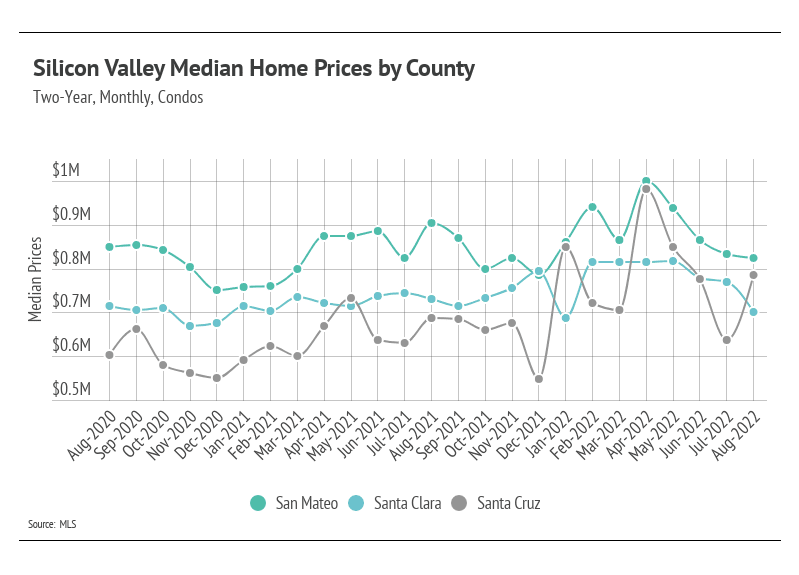

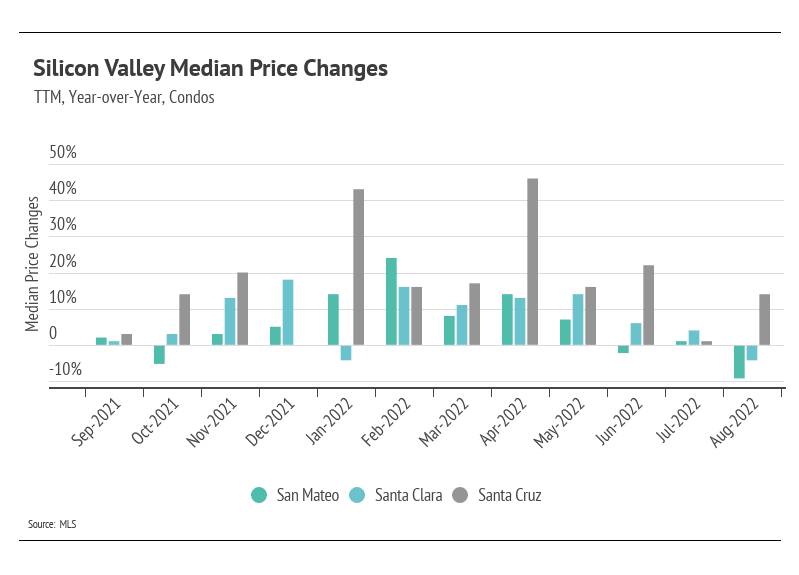

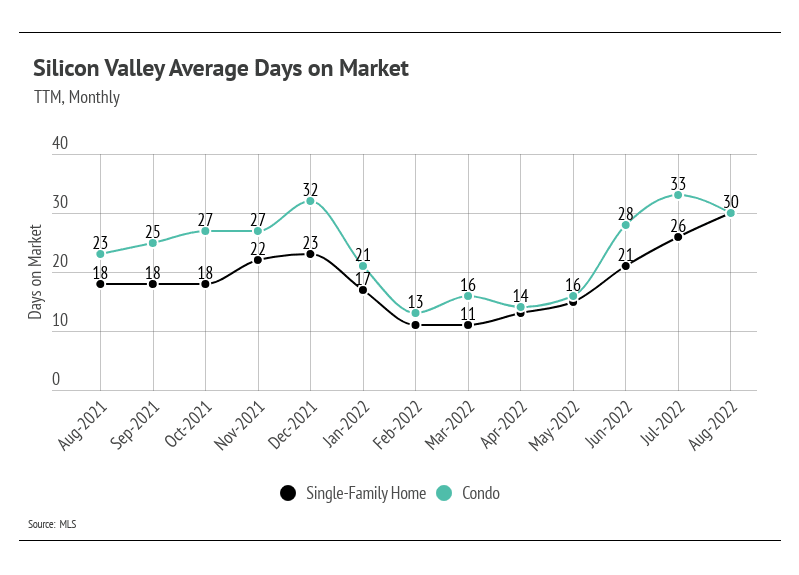

Prices tend to stagnate or decline slightly this time of year, which is exactly the case in Silicon Valley. The median single-family home and condo prices have declined off their peaks reached earlier this year. Since the peak, prices have contracted by 17% for single-family homes and 15% for condos. The price movements aren’t unexpected, as we are returning to more normal seasonal trends of price growth in the first half of the year and slight contraction in the second half. This is, of course, exacerbated by rising mortgage rates. Although the current average 30-year mortgage rate of 5.66% is still historically low, the hyper-low rates we experienced in 2020 and 2021 allowed many more buyers to enter the market. We saw firsthand what happens when demand booms in an already undersupplied market: Home prices skyrocketed. Since August 2020, single-family home prices have increased 15%, while condo prices declined slightly with the exception of Santa Cruz condos, which have increased 30%. When we link the price increases and seasonal trends with the 2.5% increase in 30-year mortgage rates, which increase the monthly mortgage payment by about 35%, we get a better picture of why sales have slowed and prices declined.

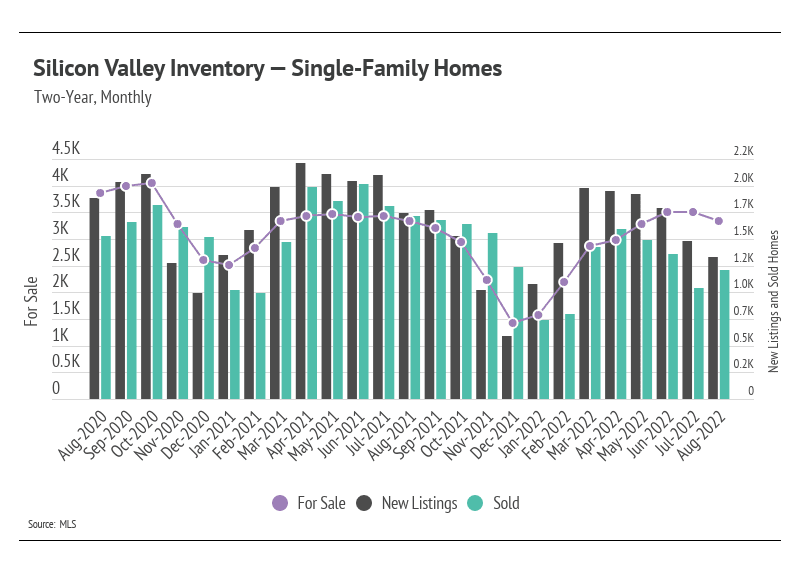

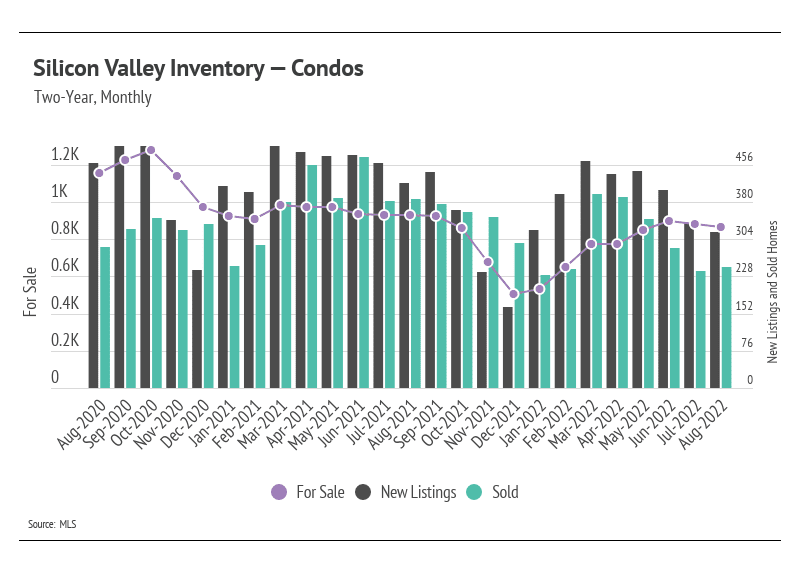

Single-family home and condo sales increased month-over-month, while new listings declined, dropping inventory for the second month in a row. The number of homes for sale has trended lower over the past three years and settled at lower levels, which is likely the new normal for housing inventory in the country. Generally, smaller supply equates to fewer sales. For example, if 500 homes sold last year, but there are only 300 homes for sale on the market this year, it’s awfully difficult to hit more than 300 sales. There were 16% fewer homes on the market in August 2022 than in August 2020. Although 2022 has had one of the lowest inventories on record, we were pleased to see that inventory is following historical seasonal trends. With the drop in inventory in August, the peak inventory level for 2022 will undoubtedly be one of the lowest on record.

Additionally, the huge number of sales in 2021 implies a sales slowdown in the future, and the future is now. On average, people move about 12 times in their lifetime in the United States, meaning if a million more people than average buy a home one year, there’s a decent chance about a million fewer people will buy a home the next. Homes are generally not something people continuously buy year after year.

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). From May to July, single-family home and condo MSI climbed higher (toward balance), but MSI fell in August, indicating we are still firmly in a sellers’ market.

Stay Updated On Our Most Recent Blog Posts

Buyer's Real Estate Tips

Thao Dang Pham | June 19, 2026

Buyer's Real Estate Tips

Thao Dang Pham | June 10, 2026

Buyer's Real Estate Tips

Brian Ng | May 28, 2026

Real Estate

Brian Ng | May 5, 2026

Real Estate

Brian Ng | April 28, 2026

Real Estate

Brian Ng | April 3, 2026

You’ve got questions and we can’t wait to answer them.