Silicon Valley Newsletter - January 2024

January 18, 2024

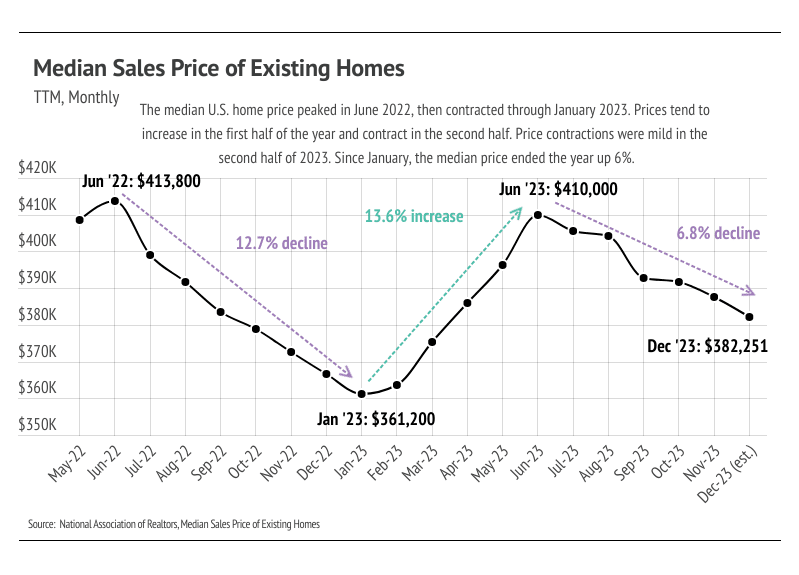

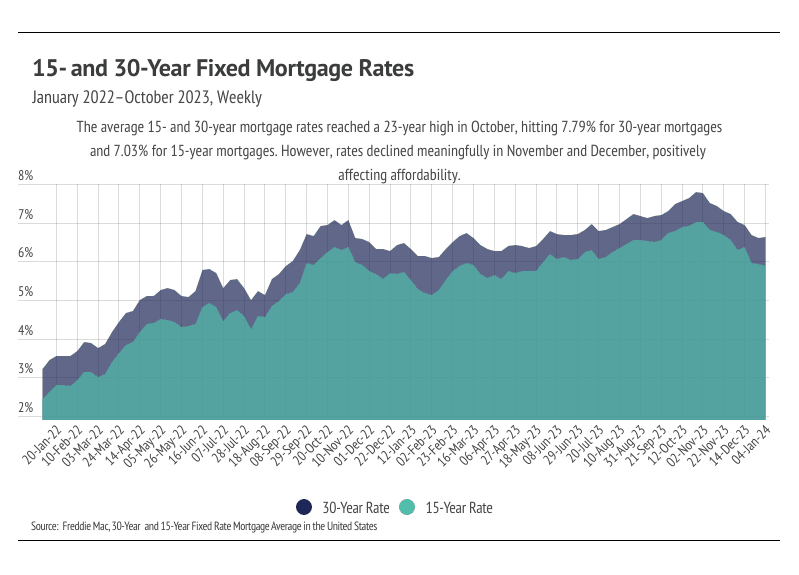

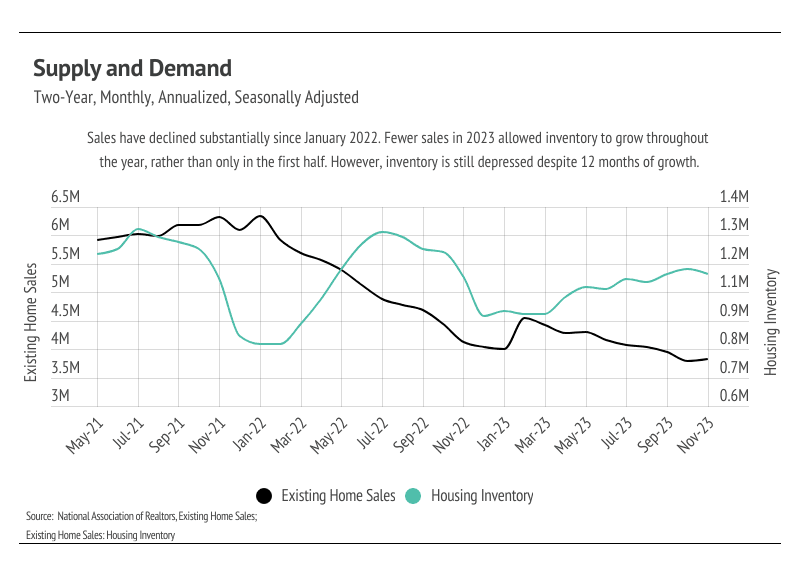

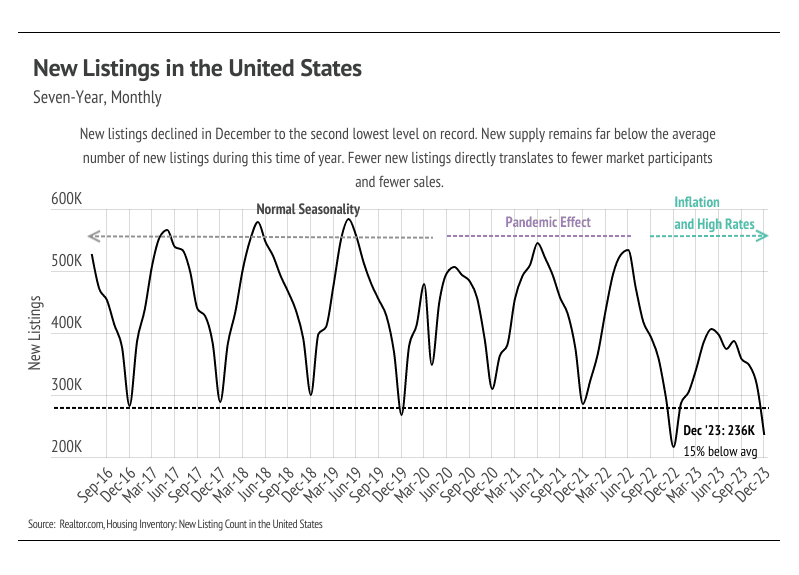

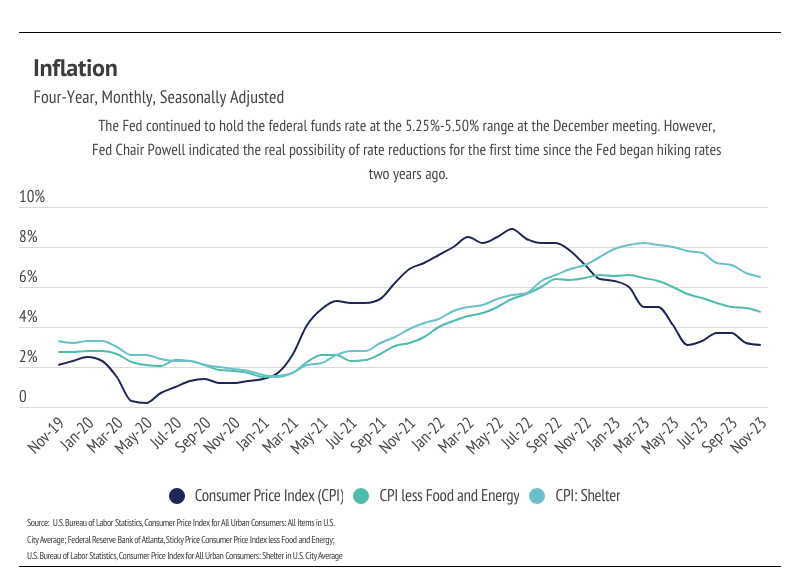

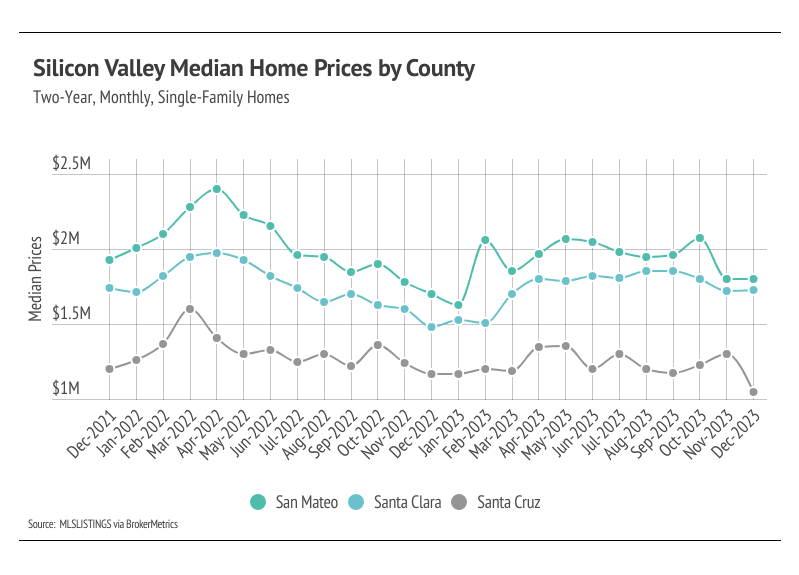

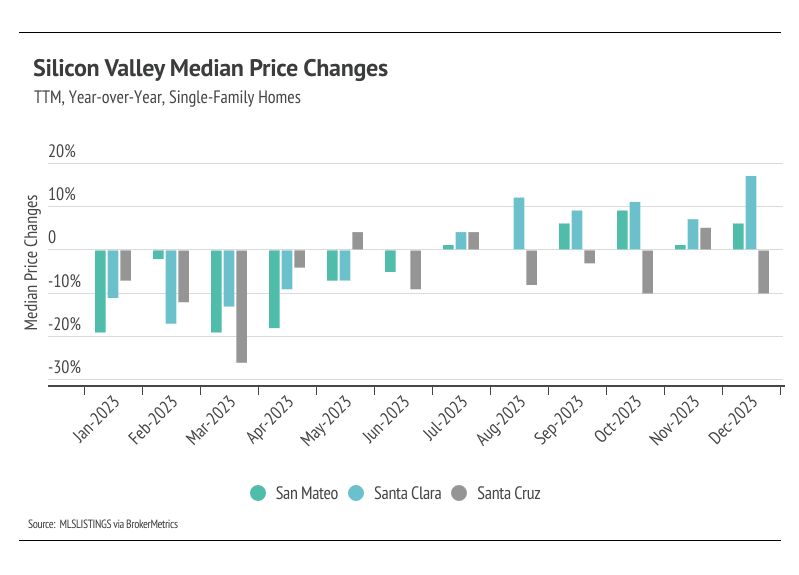

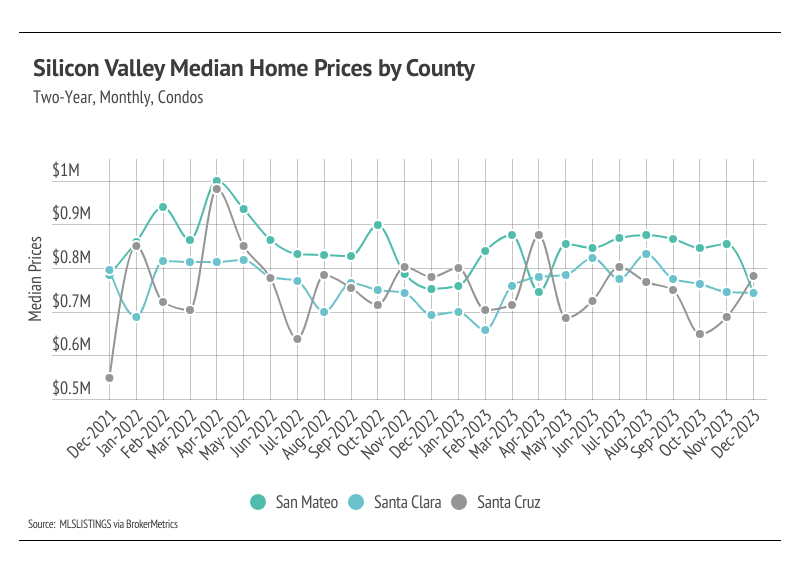

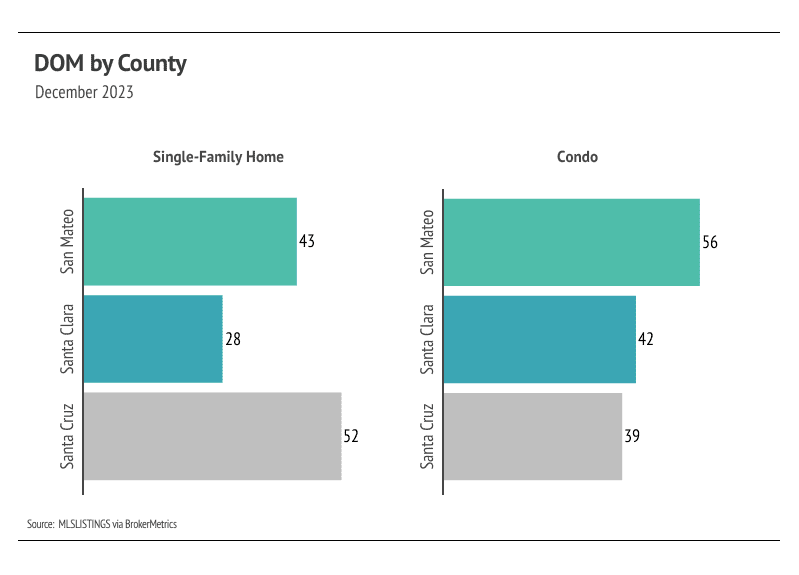

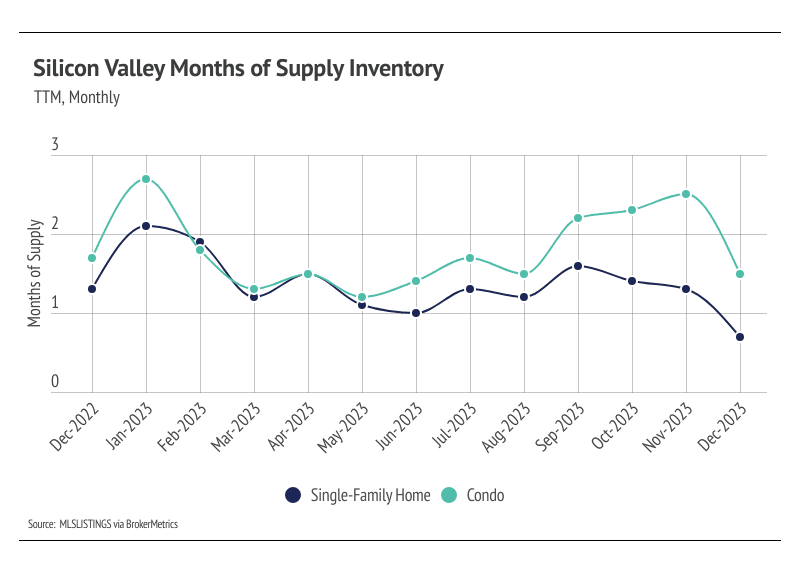

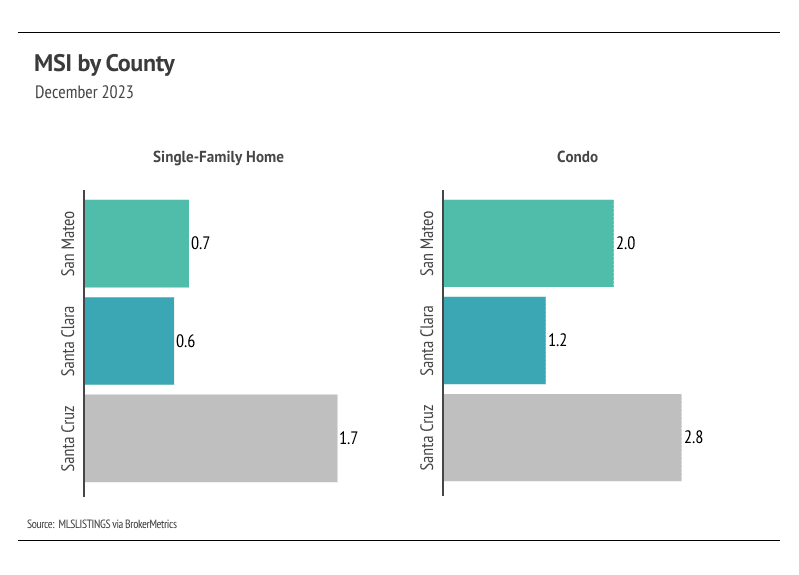

Market Update

January 18, 2024

Market Update

Stay Updated On Our Most Recent Blog Posts

Buyer's Real Estate Tips

Brian Ng | July 7, 2026

Buyer's Real Estate Tips

Brian Ng | June 30, 2026

Buyer's Real Estate Tips

Thao Dang Pham | June 19, 2026

Buyer's Real Estate Tips

Thao Dang Pham | June 10, 2026

Buyer's Real Estate Tips

Brian Ng | May 28, 2026

Real Estate

Brian Ng | May 5, 2026

You’ve got questions and we can’t wait to answer them.